Roof Repair Financing Options

Roof repair financing options make larger repairs accessible to many homeowners. National Roofing Services outlines available plans and helps you select affordable terms. Contact 303-555-7788 to discuss financing and get started. Flexible payment choices help protect your home without undue strain.

Why financing your roof repair can be a smart choice

Unexpected roof damage or deferred maintenance can turn into a major expense that many homeowners struggle to cover out of pocket. Financing your roof repair spreads the cost over time, letting you address urgent issues before they escalate and become far more costly. A timely repair protects the structure of your home, preserves energy efficiency, and prevents water intrusion that can damage insulation, drywall, and personal belongings.

Choosing a financing plan is not simply about finding money; it's about risk management and preserving home value. By committing to a manageable monthly payment, you reduce the likelihood of emergency repairs or insurance complications later on. Many homeowners find that reasonable financing allows them to select higher-quality materials and skilled labor, yielding a longer-lasting roof and better long-term value for the property.

National Roofing Services helps homeowners evaluate the real total cost of repairs, including the potential savings from addressing leaks or damaged shingles early. We'll walk through life-cycle expectations for roofing materials, local contractor options, and how financing interacts with any available insurance coverage. Our goal is to help you choose an option that protects your home without placing undue strain on your monthly budget.

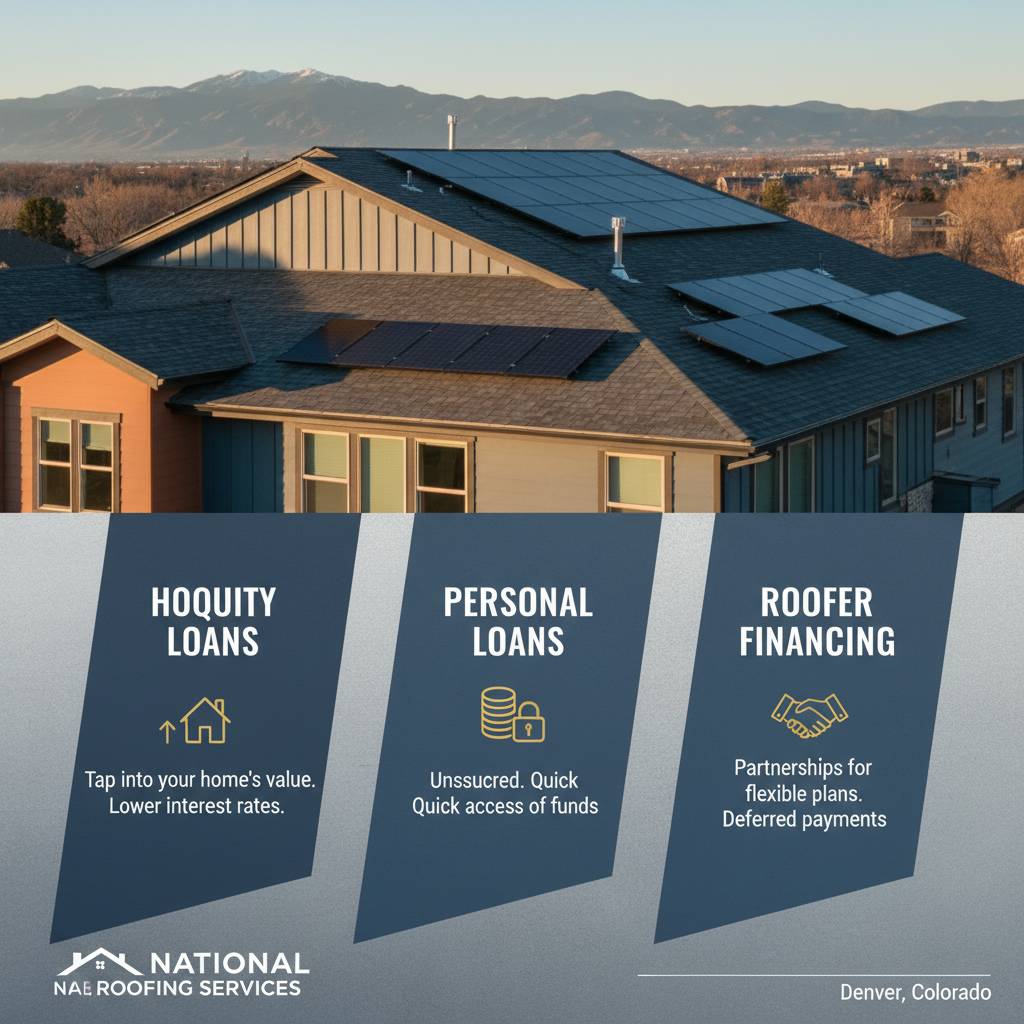

Common roof repair financing options explained

There are several well-established ways homeowners finance roof repairs, each with pros and cons. Typical choices include home equity lines of credit (HELOCs), personal loans, contractor financing plans, credit cards, and government or municipal programs in some areas. Understanding how each option affects interest, repayment terms, and the total cost over time is critical to making an informed decision.

There are several well-established ways homeowners finance roof repairs, each with pros and cons. Typical choices include home equity lines of credit (HELOCs), personal loans, contractor financing plans, credit cards, and government or municipal programs in some areas. Understanding how each option affects interest, repayment terms, and the total cost over time is critical to making an informed decision.

Below is a concise comparison of the most common options to help you weigh them quickly:

| Option | Typical Term | Interest | Best for |

|---|---|---|---|

| Home Equity Loan / HELOC | 530 years | Lower than unsecured loans (variable or fixed) | Large repairs when you want longer repayment period |

| Personal Loan | 27 years | Fixed, higher than secured loans | Moderate repairs with predictable payments |

| Contractor Financing | 6 months - 10 years | Promotional 0% or variable | Quick approvals and bundled warranties |

| Credit Card | Revolving | High unless promotional | Small repairs or short-term needs |

| Government / Local Programs | Varies | Low or subsidized | Income-qualified homeowners and energy upgrades |

Each choice interacts with credit, home equity, and future financial flexibility. For example, a HELOC can be cost-effective because of lower interest rates, but it uses your home as collateral. Contractor financing often provides convenient application and fast turnaround, but you should read the fine print for deferred interest or balloon payments. NRS can help you interpret those contract terms so you're not surprised later.

How to choose the right plan for your situation

Start by assessing the size of the repair and the urgency. Minor shingle replacement or localized flashing work may be handled with a short-term loan or even a credit card promotion, while a full roof replacement typically benefits from longer-term financing like a home equity loan or a term personal loan. Consider your monthly cash flow, anticipated future expenses, and how long you plan to remain in the home.

Next, compare the true cost of each financing route. That means looking beyond the headline interest rate and calculating the annual percentage rate (APR), total interest paid over the term, origination fees, prepayment penalties, and any requirements for down payments or deposits. If a contractor offers promotional financing, ask for a written example of total cost at the end of the promotion and whether deferred interest applies.

Timing and credit profile matter too. If you have strong credit and substantial home equity, secured options often yield the lowest rates. If you prefer to avoid putting your house at risk, an unsecured personal loan may be preferable even at a slightly higher rate. National Roofing Services will review your priorities-rate, term, monthly payment, or something else-and recommend options that align with your goals while keeping future flexibility in mind.

Questions to ask before signing any financing agreement

- What is the APR and how is it calculated?

- Are there any deferred interest terms or balloon payments?

- Is there an origination fee, application fee, or early repayment penalty?

- How long until funds are disbursed and what is the draw schedule?

- Does the loan require collateral or affect your mortgage?

Asking these specific questions up front can prevent surprises. When a contractor offers in-house financing, request the complete loan disclosure and consider getting competing offers from banks or credit unions. An objective side-by-side comparison often reveals small costs that significantly affect the long-term affordability of the project.

Application process: step-by-step and practical tips

Applying for roof repair financing typically follows a predictable sequence: estimate the cost, choose potential lenders, prepare documentation, submit applications, and review offers. Begin by getting at least two or three detailed repair estimates so lenders understand the scope and cost of the work. This documentation often speeds approvals for home improvement loans and contractor financing alike.

Applying for roof repair financing typically follows a predictable sequence: estimate the cost, choose potential lenders, prepare documentation, submit applications, and review offers. Begin by getting at least two or three detailed repair estimates so lenders understand the scope and cost of the work. This documentation often speeds approvals for home improvement loans and contractor financing alike.

Organize the paperwork lenders commonly request: proof of income, recent tax returns, a copy of your homeowners insurance policy, and a detailed contractor estimate or contract. If you're applying for a HELOC or home equity loan, be prepared for an appraisal and title documentation. Conservatively evaluate your ability to handle monthly payments and include maintenance reserves so repairs don't push your household budget to the limit.

Here are practical tips that reduce friction during approval:

- Check your credit score early and correct any errors on your credit report.

- Ask the contractor if they will work with multiple lenders or provide paperwork for loan disbursement.

- Compare full disclosures rather than headline rates; focus on APR and total cost.

- Get timelines for when funds are required and when the contractor will start work.

Balancing cost, coverage, and contractor selection

Financing the repair is only part of the equation; the quality and reliability of the contractor are equally important. A lower financing cost is less valuable if the contractor performs poor work or fails to honor warranties. Request proof of licensing, liability insurance, and references. Ask for a clear contract that lists materials, timelines, milestones, and warranty terms-these items matter when lenders disburse funds for the job.

Financing the repair is only part of the equation; the quality and reliability of the contractor are equally important. A lower financing cost is less valuable if the contractor performs poor work or fails to honor warranties. Request proof of licensing, liability insurance, and references. Ask for a clear contract that lists materials, timelines, milestones, and warranty terms-these items matter when lenders disburse funds for the job.

Consider structuring payments around project milestones rather than paying everything upfront. Many reputable contractors will accept partial payment at the start, a mid-project draw, and a final payment upon completion and inspection. This arrangement provides an additional layer of accountability and protects both parties while still fitting naturally into most financing plans.

When evaluating proposals, weigh the expected lifespan of materials against the financing term. It often makes sense to align the loan term with the durable life of the new roof-for instance, financing a 25-year roofing system with a loan that spreads payments over a significant portion of that time-so you enhance value and avoid outsized short-term debt for a long-lived asset.

Addressing common concerns and frequently asked questions

Many homeowners worry that financing will be prohibitively expensive or that they may lose flexibility. While those are valid concerns, informed decisions and comparison shopping typically produce a plan that balances monthly affordability with total cost. If you anticipate moving in the near term, choose shorter financing or options that do not tie up your home's equity.

Many homeowners worry that financing will be prohibitively expensive or that they may lose flexibility. While those are valid concerns, informed decisions and comparison shopping typically produce a plan that balances monthly affordability with total cost. If you anticipate moving in the near term, choose shorter financing or options that do not tie up your home's equity.

Insurance is another common question. If damage is due to a storm or covered peril, your homeowners insurance may pay for a significant portion of the repair. However, deductibles and coverage limits vary, and insurance claims can be time-consuming. Financing can bridge the gap between insurance payouts and contractor invoices, letting the work proceed efficiently while the claim is processed.

Below are a few quick FAQs:

- Will financing affect my ability to refinance my mortgage? It depends on the product-secured loans may impact future mortgage decisions, so consult your lender.

- Can I use a short-term credit option for a full roof replacement? Technically yes, but interest costs may be high unless you can pay the balance quickly.

- Is contractor financing safe? It can be when offered by reputable lenders; always get full disclosures and compare with outside offers.

Case studies and real-world examples

Case study 1: A family discovered multiple roof leaks after a severe storm. They used a contractor's promotional 12-month 0% financing to complete repairs immediately and then refinanced into a low-rate personal loan with a 5-year term once their insurance payout arrived. This approach minimized delay and avoided additional interior damage, while keeping monthly payments within budget.

Case study 1: A family discovered multiple roof leaks after a severe storm. They used a contractor's promotional 12-month 0% financing to complete repairs immediately and then refinanced into a low-rate personal loan with a 5-year term once their insurance payout arrived. This approach minimized delay and avoided additional interior damage, while keeping monthly payments within budget.

Case study 2: A homeowner needed a full roof replacement but preferred not to use home equity. They secured a fixed-rate personal loan with a seven-year term, enabling them to choose higher-grade shingles and enroll in a roofing warranty. The predictable monthly payment and fixed rate provided peace of mind and preserved their home equity for future needs.

Each homeowner's situation is unique; these examples illustrate how different financing paths can be tailored to match priorities-speed, low monthly payments, or preservation of home equity. National Roofing Services can review similar scenarios and recommend the most realistic paths for your circumstances.

Next steps and how National Roofing Services can help

Deciding to finance a roof repair is a proactive move to protect your home and investment. Start with a no-obligation consultation to assess the damage, collect contractor estimates, and review financing options that fit your credit profile and budget. National Roofing Services advises on documents you'll need and helps compare offers so you can choose the plan that minimizes cost without sacrificing quality.

We're ready to answer detailed questions about loan terms, contractor protections, and how to coordinate insurance and financing for the smoothest possible repair process. If you're unclear about any loan disclosure or contractor clause, bring them to us-we'll explain or negotiate terms when possible, so you move forward confidently.

Call to action: For tailored guidance on roof repair financing options and to explore payment plans that suit your needs, contact National Roofing Services today. Speak with an experienced representative who will walk you through options and connect you with reliable contractors and lenders.

Call now: 303-555-7788

We look forward to helping you protect your home with an affordable, well-structured financing plan. Contact National Roofing Services at 303-555-7788 to get started and get peace of mind from a sound repair strategy.